Dragons' Teeth: The German Chancellor, Angela Merkel's, torture of Greece marks the end of the European project. Europe's acquiescence at Versailles in 1919 meant that, within 20 years, Europe was, once again, at war with itself. The EU's refusal to stand in solidarity with the Greeks against German aggression (deploying banks this time, not tanks) has set the continent on the path to ever-increasing conflict and economic sclerosis.

Once all the Germans

were warlike and mean

But that couldn’t

happen again.

We taught them a

lesson in 1918

And they’ve hardly

bothered us since then!

YANIS VAROUFAKIS openly compares the Eurozone’s diktat to Greece with the Treaty of

Versailles. The former finance minister’s comparison is well made. The

Carthaginian peace imposed upon the German people in 1919 was not only intended

to devastate their economy it was supposed to crush their spirit.

As punishment for launching the most catastrophic military

conflict in human history, the Germans were to be kept in a state of economic

servitude for decades to come. Nor was the victorious allies claim that Germany

was solely responsible for the outbreak of the First World War a matter of mere

rhetoric. The British naval blockade of Germany, which was gradually starving

the defeated nation to death, would not be lifted until Germany’s “negotiators”

(not that these were, in any genuine sense, negotiations) accepted the Treaty’s

“War Guilt Clause”.

As the brutally punitive intentions of the Versailles diktat gradually emerged, three members

of the Imperial British delegation, Harold Nicolson, Jan Smuts and John Maynard

Keynes were filled with a terrible sense of foreboding. All three were

convinced that nothing good could come from such an inhuman document. Each

understood, with a chilling certainty, that the victorious allies were sowing

dragons' teeth.

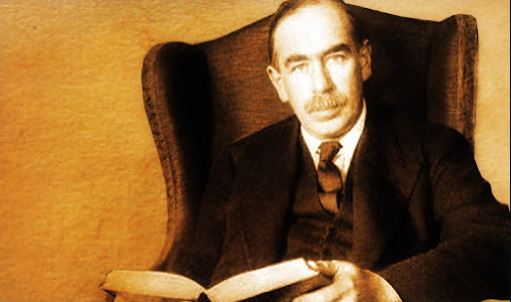

John Maynard Keynes: A terrible sense of foreboding.

The young economist, Keynes, quit the negotiations and

returned to England where he spent the summer months of 1919 writing The Economic Consequences of the Peace.

In his book (which instantly became an international best-seller) Keynes argued

that the massive reparations demanded of Germany, combined with the Americans’

insistence that all Allied war debts be repaid, could only result in a

fundamental derangement of the global economy. Throw in the German people’s

Versailles-inspired sense of grievance and disaster was guaranteed. With

uncanny accuracy, he predicted that Europe would be at war with itself, again,

in just 20 years.

Flogging A Dead Horse: The imposition, by the victorious allies of World War I, of impossibly harsh economic conditions on the German people, constituted the first step on the road to World War II.

Of course, Greece is not Germany. Her people are not about

to pull on jackboots and stomp all over the peace of Europe. But Germany is Germany and it is nothing short of

tragic that the nation that went through the experience of Versailles – and all

that followed from it – has so easily forgotten how it feels to be ganged-up on

by a Europe determined to drive your country to the wall economically and strip

it of what little self-respect it has managed to retain.

This failure of memory is particularly worrying in the light

of what happened in 1953. That was the year in which Germany’s European

neighbours, including Greece, wrote off up to 50 percent of her still

outstanding Versailles debts. Yes, it was the Cold War. Yes, Germany was

divided and it was important to give those Germans living in the West a sense

of hope and confidence in the future. Even so, barely 14 years had passed

since, as Mick Jagger put it: “the blitzkrieg raged/and the bodies stank”.

Europe had considerably more to forgive Germany for in 1953 than it has to

forgive Greece for in 2015.

Germany's Angela Merkel and Wolfgang Schauble: Executioners of the European dream.

The spectacle of Germany’s Chancellor, Angela Merkel, and

her flinty-faced Finance Minister, Dr Wolfgang Schauble, squeezing the last drops

of blood from the broken stones of Greece has sent a collective shudder through

the rest of Europe. It’s a reaction with which Dr Schauble will be well

pleased. It has long been the German Finance Minister’s plan to render

Germany’s economic hegemony over Europe permanent by turning the continent into

a “glorified debtors’ prison”. Greece is to serve as an example of what will befall any

Eurozone member foolhardy enough to challenge the one-way flow of wealth to

Europe’s biggest banker.

Frau Merkel is convinced that by allowing Greece to remain

in the Eurozone she has demonstrated her bona fides as a “Good European”. It

is, after all, vital that all Europeans understand that debts must be repaid,

and that only orthodox economic policies should be pursued. If that requires

German technocrats to second-guess the decisions of elected Greek politicians,

then so be it. The Greek people need to understand that democracy has its

limits; that saying “No” has a price.

The economic consequences of Angela Merkel, like the economic

consequences of Versailles, will be a Europe at war with itself – within 20

years.

This essay was

originally published in The Waikato Times, The Taranaki Daily News, The

Timaru Herald, The Otago Daily Times and The Greymouth Star of Friday, 17 July 2015.